Fed Reversal Pricing

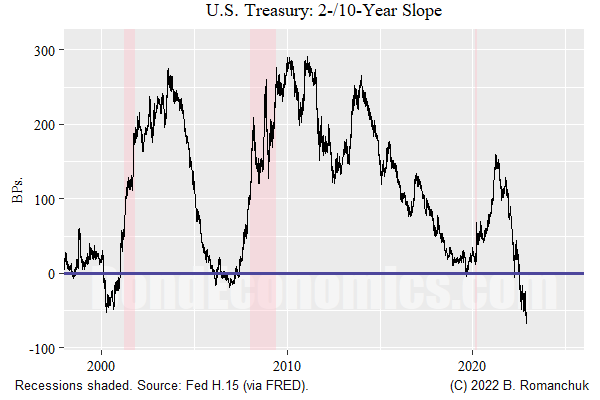

The 2-/10-year curve has reached “modern record” levels of inversion in the recent days. Although the usual interpretation of this event is that it is a recession indicator, it is more accurately thought of as a “Fed reversal” indicator. However, that distinction is somewhat academic, since the Fed normally reverses course during recessions.

Note: I am now on Mastodon: https://econtwitter.net/@RomanchukBrian. Since I am not following accounts posting silly cat videos (yet), my Mastodon feed is going to be more “serious” than my Twitter content. I will treat my Mastodon feed as I did my Twitter feed when I started — mainly tweeting links to economic/financial content that I have read or written. Given my aversion to American culture war issues, I might transition more towards Mastodon to avoid expected problems on Twitter during the two-year Presidential election campaign.

The inversion of the 2-/10-year curve was inevitable given the Fed’s reaction function: they are hiking rates in response to inflation — a lagging economic indicator. Even if the terminal Fed Funds rate is revised higher due to positive inflation/growth surprises, the curve will tend to move somewhat in parallel, allowing the 10-year yield to remain below the 2-year. A bear steepener would require expected rate hikes to weight more heavily on forward rates beyond the 2-year point, which is unlikely to happen at this stage of the cycle. (Bear steepener stories are more plausible if the central bank is reacting or hiking slowly, locking down the 2-year leg of the slope.)

Other Indicators?

If one is an outside observer, using the Treasury yield curve as a generic “indicator” for recession odds makes sense. But doing so obscures one issue: where does the “indicator” come from? If one is an academic economist, one can mumble something about “equilibrium” and argue that bond prices magically appear out of the laws of economic nature. Although large masses of smaller players (e.g., mortgage borrowers) will eventually weigh on the market, near run pricing is determined by large actors attempting to maximise their trading profits. At least some of those actors will trade the yield curve slopes relative to where they see the odds of scenarios like a Fed reversal — and so they need to develop odds of those scenarios without using the yield curve as an indicator.

I am certainly not on top of the economic data flow. However, I did a scan of data that I have access to, and there was not a lot of series that were as suggestive of a serious deterioration of the economy as the 2-/10-year slope. One of the most “exciting” charts I saw was the New York Fed’s business survey (above). Although it has dropped below zero, I am not the greatest fan of the usefulness of this series.

Right now, the coincident data is consistent with the U.S. economy muddling along. Although I cannot rule out a recession in 2023, that is not saying very much.

Causality Via Banks?

I ran into a comment that yield curve inversion is a causal factor for recessions. (Since I do not want to address the entire argument made, I will not quote the original source.) The story appears straightforward: banks (allegedly) lend long term and borrow short term, and so the curve inversion reduces net interest margins and makes it unattractive to lend, which will then dampen growth rates.

This is a relatively large topic (that I have ranted about previously). I will address it in a stand alone article shortly, since it is a common enough story to warrant treatment in my banking book.

As a spoiler, I will just note that this “borrow short/lend long” story requires banks to run a duration mismatch. Historically, these mismatches happened — the Savings and Loan (S&L) Crisis in the United States was a long-term consequence of the Savings and Loan industry getting trashed by Volcker’s rate hikes. (The big idea to deal with those earnings issues was to allow the S&L’s to take more credit risk, which then led to dubious lenders expanding with the help of “captured” politicians.) However, the Bond Market Armageddon of 1994 led regulators and banks to embrace monitoring duration risk.