Central Banking Confusion

The Fed and Bank of Canada announced that they were on hold yesterday, but signalled that rate hikes are likely hitting in March. From what I have seen of chatter on Twitter and various editorial pieces, this has caused some confusion. (I am not sure what street research is saying.) This article is a grab bag discussing what I saw as common (or at least popular) points of confusion, as well as some of my editorial comments.

Editorial: Yeah, That Stochastic Calculus Really Helps

Most people are quite reasonably not concerned about economic theory disputes most of the time. But one needs to keep them in mind when keeping up with the latest events.

Whenever you are reading commentaries about central banking outlooks, you need to ask yourself: are the people in the discussions using any of the mathematical models that the literally thousands of neoclassical doctorates employed by the central banks produced? If not, what exactly was the point of them? Why is it so important that MMT have lots of mathematical models of the economy (keeping in mind that critics ignore the ones that exist) when nobody even refers to the ones that are supposed to be relevant?

Admittedly, one might not expect equity or credit analysts (or gold bugs) to keep up with DSGE modelling, but rates analysts — the primary target for rates discussions, allegedly — almost all have science/mathematical doctorates from fancy universities. If the models worked, the technical audience to use them is there. However, the only people interested in those models are those whose credentials are tied to the production of said models, which is not encouraging.

(Probably) No Need For 50 Basis Point Hikes

I do not have access to a plot of the instantaneous forward rate, but the figure above is my best bet what the shape looks like for forwards up to ten years or so. (The instantaneous forward rate is the implied path of the overnight rate from a fitted discount or zero curve.) After the ten year point, you are fitting less liquid bonds, and there are various technical effects that impact the shape of the curve. For example, you typically see a hump in the curve due to the value of convexity, which implies an inversion of some forwards. See my earlier article on the long end inversion for more details. Bonds with maturities under ten years do not have a lot of convexity, so the hump is pushed out beyond that point.

As an aside, different sources will legitimately have different instantaneous forward curves. The instantaneous forward curve is determined by taking the derivative of the discount curve, and so different choices for parameterising the zero/discount curve will result in quite different forward curves. To price an instrument with a duration longer than overnight, you take the geometric mean of the instantaneous forwards over the life of the instrument. This “integrating out” of the forward curve will mean that different fits will end up with roughly the same fair value prices of traded instruments.

The figure shows the actual instantaneous curve, along with straight line approximation. I divided the straight line approximation into three regions, labelled A to C.

Region A is the “on hold” period. The forwards are relatively flat, possibly with a small term premium effect.

Region B is the “hiking period” which features the most rapid change in the forward rate per unit of forward time. In the modern era, it’s a good bet that the “slope” of that line will be a multiple of 25 basis points / (k × six weeks), with k in the set 1, 2, …. The six weeks is the number of central bank policy meetings per year, so that is 25 basis points every k meetings.

Region C is the “terminal rate” period where the forward rises at a very slow pace. One possible interpretation is that the observed forward is the “terminal rate” plus a term premium.

We can then write a the fair value yield of a bond as follows:

yield = f(length of on hold period, slope of hiking period, terminal rate, term premium).

Since the term premium is just going to generate arguments, we can replace the “terminal rate” with the “adjusted terminal rate,” where the adjustment is to add the average term premium.

We can then ask: what matters for bond yields? Well, if the hiking period is two years, eight years of a 10-year bond’s lifetime has the instantaneous forward rate equalling the “term premium adjusted” terminal rate. That is 80% of the observed yield is explained by the terminal rate. The rate of initial hiking does not matter too much, all that matters is that it reaches the terminal rate relatively quickly.

At 25 bps/meeting, the policy rate is rising at 200 basis points per year. That puts us at 4% in two years, which seems be hawkish enough when compared to past history (figure above). The only conceivable reason to go to 50 bps/meeting is that the policy rate needs to be 6% or so very quickly — which seems to be a bit of a stretch.

As was pointed out by Ben Bernanke (possibly the “Gradualism” speech), the Fed Funds rate (or any overnight risk free rate) is only of limited importance for the real economy. Non-financial entities borrow and invest quite often at term rates, and if rates are rising, they will be cautious about borrowing overnight.

The real battle between bond bulls and bears is where to plant the terminal rate. At current pricing, 25 bps/meeting is enough to vaporise the bulls.

Why Not One And Done?

The idea of doing one big hike and getting it over with recurs over time. Two cycles ago, Stephen Roach floated the idea in a op ed, which was answered by the Bernanke “gradualism” speech. (Although not a Bernanke fan, I think that speech was a very good explanation of conventional central bank thinking. It also referred to “bang-bang control,” which I ran into during my doctoral student days.)

The argument against it is very straightforward. Let us assume that we follow conventional beliefs about interest rates (higher policy rates act to suppress growth and/or inflation). But if we are faced with uncertainty, the safest course of action is to move the policy rate gradually, and then change direction/go on hold when the trend in the economy is changing. “Doing it all at once” relies on a belief that we know what the terminal rate is. The current set up frees central bankers from having to forecast the terminal rate: that’s the job of rates market participants. The central bank just ratifies spot overnight pricing.

Since the effect of interest rates is determined by levels along the whole curve, a higher implied terminal rate still has an immediate effect.

“The” Interest Rate Dial Does Not Exist

I ran into some comments by someone attempting to make a big deal about the flattening that occurs during a tightening cycle. The idea is that since other rates (allegedly) matter more than the overnight rate, then the market is counter-acting the policy rate rise.

I would argue that this is a symptom of using Economics 101 models with one “interest rate.” Any modern models tell us that the yield curve is a continuum, and the only way to make sense of pricing is that yields are primarily determined by expectations.

The curve does not move in parallel with the overnight rate. You cannot expect X basis points in hikes to translate into an X basis point rise in yields/rates across the maturity spectrum. If you are attempting to measure the effect of interest rates on the economy (good luck), you probably need to somehow capture the levels across the curve, and not use the policy rate as a proxy.

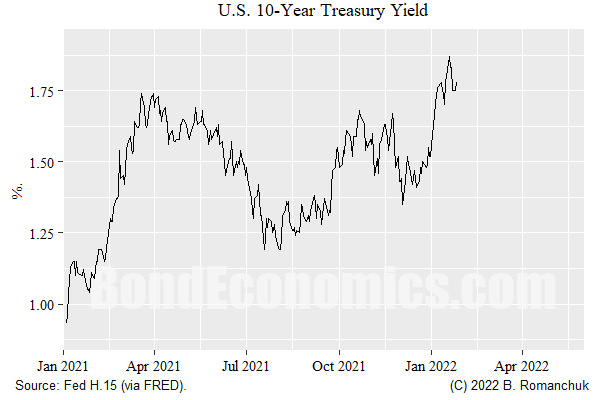

Since markets are forward looking, the timing of trend changes in yields will not match the timing of changes in administered rates. Given that markets with levered players invariably overshoot in both directions, it is completely unsurprising that bond bear markets happen before the first hike, and rally once it hits. You need to look at the yield levels, and the current 10-year yield is higher than it was during most of 2021 (figure above); hence the “interest rate tightening” has started already.